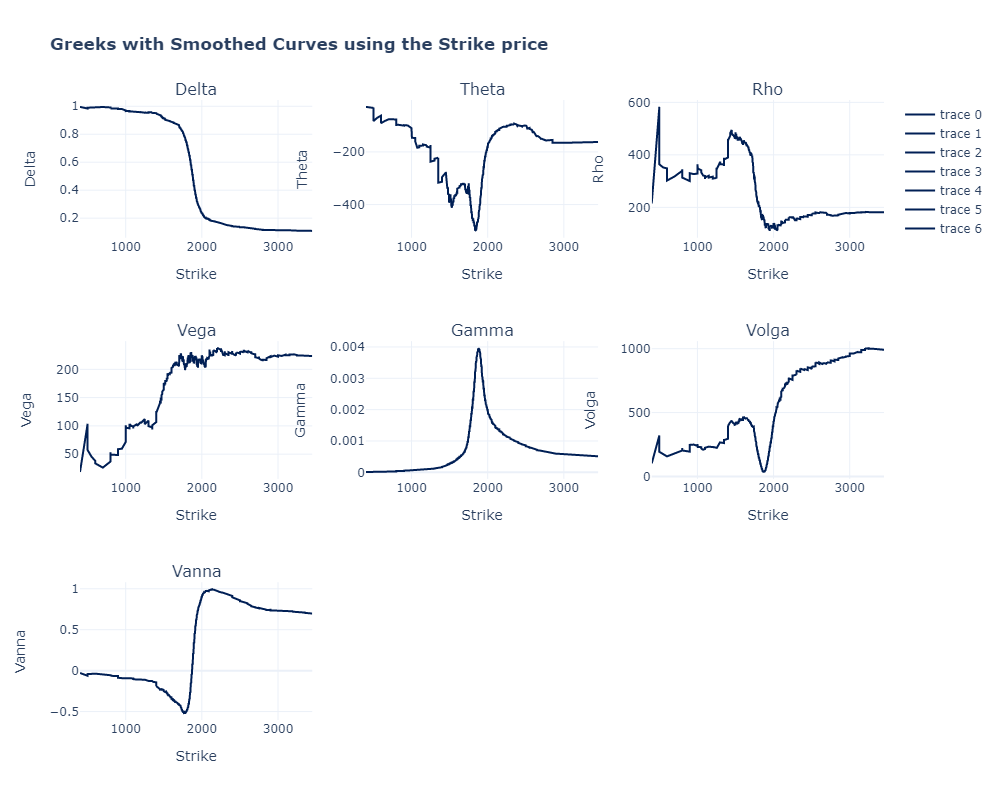

Analysis of Russell 2000 options data using web scrapping and the Black and Scholes model06/04/2023Learn more

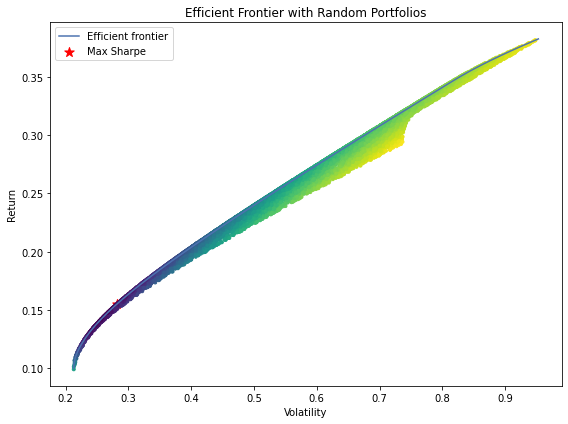

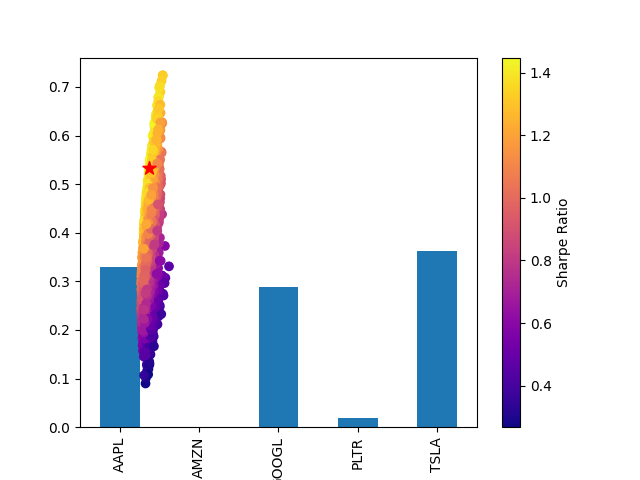

Portfolio optimization using the mean variance framework of Markowitz, efficient CVaR and efficient CDaR optimizations01/05/2023Learn more

.png)